Down Payment Chester County PA: How Much Do You Need to Buy a Home in 2026

One of the first questions I get from buyers in Chester County PA is about down payment. How much do I actually need? Do I have to put 20 percent down? What if I do not have a lot saved?

The good news is that the 20 percent down payment rule is a myth for most buyers. The reality in Chester County PA is that your down payment depends on the loan program you use, your credit score, and your specific financial situation. Some buyers put down 20 percent. Others put down 3 percent. Some put down nothing at all.

This guide breaks down exactly what every loan program requires, what closing costs look like on top of the down payment, and what the full cash to close number actually looks like at real Chester County price points in 2026.

The 20 Percent Myth: What You Actually Need for a Down Payment in Chester County PA

For decades buyers have been told they need 20 percent down to buy a home. That is simply not true for most people.

Twenty percent down eliminates private mortgage insurance, which is a real benefit. But it is not a requirement. Most loan programs allow significantly lower down payments and many first-time buyers in Chester County are closing on homes with far less than 20 percent saved.

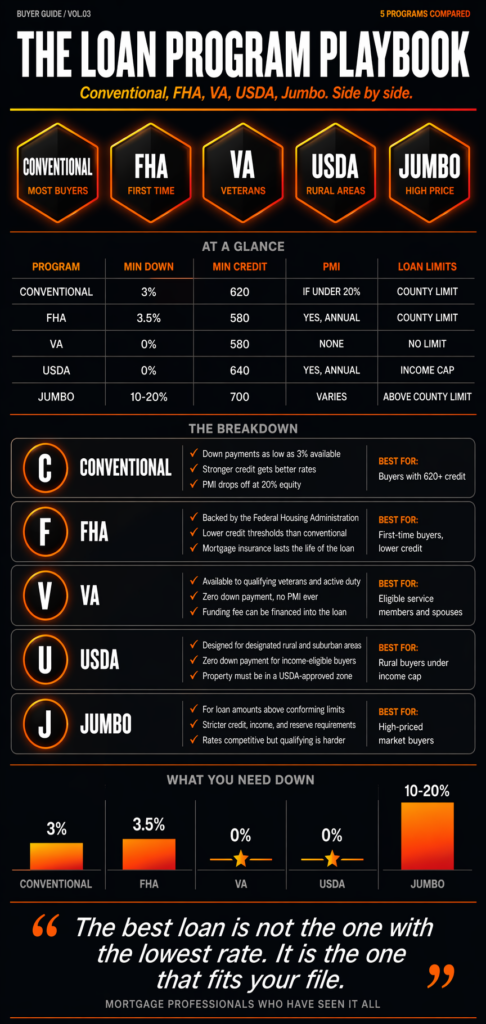

Here is the real picture by loan program.

Conventional Loans: 3 to 20 percent down

Conventional loans are the most common loan type in Chester County. They require as little as 3 percent down for qualified first-time buyers and 5 percent down for repeat buyers in most cases.

The trade-off for putting less than 20 percent down on a conventional loan is private mortgage insurance, or PMI. PMI is a monthly cost added to your payment until you reach 20 percent equity in the home. On a $500,000 purchase with 5 percent down, PMI typically runs between $100 and $200 per month depending on your credit score and lender.

The good news is that PMI cancels automatically once you hit 20 percent equity. It is not permanent. And with Chester County home values appreciating consistently, many buyers reach that threshold faster than they expect through a combination of principal paydown and appreciation.

For a full breakdown of conventional loan requirements in this market, see our conventional loans Chester County page.

FHA Loans: 3.5 percent down

FHA loans allow a down payment of just 3.5 percent for buyers with a credit score of 580 or above. For a $450,000 home that means roughly $15,750 down before closing costs.

FHA is a solid option for first-time buyers who are still building their credit profile or who have not yet saved a large down payment. The trade-off is mortgage insurance that works differently than conventional PMI. FHA mortgage insurance includes an upfront premium of 1.75 percent of the loan amount added to the loan balance, plus an annual premium paid monthly. For most FHA loans today, that insurance stays for the life of the loan unless you refinance into conventional financing later.

One thing to know about FHA in Chester County specifically. In multiple offer situations, sellers and their agents sometimes view FHA offers less favorably than conventional offers because of FHA property condition requirements. In lighter competition markets like Coatesville or western Chester County, this matters less. In tight competition markets like West Chester or Exton, it is worth discussing strategy with your mortgage broker before you decide which program to lead with.

VA Loans: Zero down payment

If you are an eligible veteran or active-duty service member, VA loans are the most powerful program available to you. No down payment required. No monthly mortgage insurance. Competitive rates that often come in below conventional pricing.

For Chester County veterans buying in the $500,000 to $800,000 range, the savings from a VA loan versus a conventional loan with 5 percent down can be significant. If you have served, this is the first conversation we have.

VA loans do have a funding fee that most borrowers pay at closing or roll into the loan, but for most veterans the overall cost is still lower than alternatives requiring mortgage insurance. Veterans with a service-connected disability rating may be exempt from the funding fee entirely.

USDA Loans: Zero down payment

USDA Rural Development loans offer zero down payment financing for eligible buyers in designated rural areas. In Chester County, properties in and around communities like Avondale, West Grove, Oxford, and Kennett Square may qualify depending on the specific address and household income limits.

If you are buying in southern or western Chester County and have not checked USDA eligibility, it is worth a conversation. For buyers who qualify it eliminates the down payment requirement entirely on a fixed-rate loan. That is a meaningful advantage for buyers who have strong income and credit but have not yet saved a large lump sum.

See our best areas for first-time buyers in Chester County for a breakdown of which communities have the strongest USDA opportunity.

Jumbo Loans: Typically 10 to 20 percent down

With Chester County’s median home price running around $526,000 in early 2026 and West Chester Borough averaging above $700,000, a meaningful number of buyers are shopping in jumbo territory. The 2026 conforming loan limit is $832,750 for a single-family home. Loans above that limit are jumbo loans and carry their own down payment requirements.

Most jumbo programs require at least 10 percent down and many prefer 20 percent. Credit requirements are also tighter, typically 700 or above. For buyers looking at Devon, Malvern, or higher-end West Chester properties, planning your down payment strategy around jumbo guidelines from the start saves a lot of frustration later.

See our jumbo loan options page for more detail on what these programs look like in this market.

Closing Costs: The Number Most Buyers Forget to Plan For

Down payment is only part of the cash you need to close on a home in Chester County. Closing costs are separate and they can catch buyers off guard if they have not planned for them.

Here is what closing costs typically include in Pennsylvania:

Lender fees cover origination charges, underwriting, and processing. These vary by lender and loan type.

Title insurance and settlement fees cover the title search, title insurance policies, and the settlement company’s work. In Pennsylvania, both a lender’s policy and owner’s policy are standard.

Pennsylvania transfer tax is one of the bigger closing cost items in this state. Pennsylvania charges a transfer tax of 2 percent of the purchase price. In most Chester County transactions that cost is split between buyer and seller, meaning the buyer typically pays 1 percent. On a $500,000 purchase that is $5,000 just in transfer tax for the buyer’s portion.

Prepaid items and escrows include homeowners insurance, the first year’s premium often paid at closing, plus an initial escrow deposit for property taxes and insurance. Depending on the time of year you close, your escrow setup can be a significant upfront cost.

Inspection and appraisal fees are typically paid outside of closing but are part of your out-of-pocket costs during the transaction.

In Chester County, total closing costs for a buyer typically run between 2 and 4 percent of the purchase price depending on the loan type, the property, and how costs are negotiated with the seller.

For a $500,000 purchase that means planning for roughly $10,000 to $20,000 in closing costs on top of your down payment.

For a detailed look at what cash to close looks like at specific Chester County price points, see our home affordability guide for Chester County.

What Does Total Cash to Close Look Like in Chester County?

Here is a realistic look at what buyers at common Chester County price points need to have ready for closing. All figures are estimates and will vary based on loan program, credit profile, and negotiated terms.

$375,000 purchase (Coatesville, Oxford, West Grove range)

Conventional 3 percent down: $11,250 down plus $7,500 to $15,000 in closing costs. Total cash to close approximately $19,000 to $26,000.

FHA 3.5 percent down: $13,125 down plus $7,500 to $15,000 in closing costs. Total cash to close approximately $21,000 to $28,000.

USDA zero down if eligible: Closing costs only. Total cash to close approximately $7,500 to $12,000 depending on seller concessions and time of year.

$500,000 purchase (Phoenixville, Downingtown, Kennett Square range)

Conventional 5 percent down: $25,000 down plus $10,000 to $20,000 in closing costs. Total cash to close approximately $35,000 to $45,000.

Conventional 10 percent down: $50,000 down plus $10,000 to $20,000 in closing costs. Total cash to close approximately $60,000 to $70,000.

VA zero down if eligible: Closing costs only plus funding fee if applicable. Total cash to close approximately $10,000 to $18,000.

$650,000 purchase (West Chester, Exton, Malvern range)

Conventional 10 percent down: $65,000 down plus $13,000 to $26,000 in closing costs. Total cash to close approximately $78,000 to $91,000.

Conventional 20 percent down: $130,000 down plus closing costs. Eliminates PMI and typically results in better rate pricing.

These are real numbers. Not estimates pulled from a national calculator. Chester County property taxes vary significantly by township and that variation can add hundreds of dollars to your monthly payment depending on where the property sits. I always work through property-specific payment calculations with buyers before we finalize an approval. A home listed at $550,000 in one township can carry a meaningfully different monthly payment than a home at the same price a few miles away.

Down Payment Assistance Options in Chester County

If saving the full down payment feels out of reach right now, there are programs designed to help. The key is knowing which ones apply to your situation.

Fannie Mae HomeReady and Freddie Mac Home Possible are conventional loan programs with expanded eligibility for buyers at or below area median income. Both allow 3 percent down and include more flexible income calculation guidelines that can help buyers in multi-generational households or buyers with non-traditional income sources.

Pennsylvania Housing Finance Agency programs offer down payment and closing cost assistance for eligible buyers across the state. Income and purchase price limits apply. These programs change periodically so the best way to know what is currently available is to have a direct conversation with a mortgage broker who is actively working with these programs.

Seller concessions are not a grant program but they are one of the most underutilized tools available to buyers in Chester County right now. In markets like Coatesville and parts of western Chester County where competition is lighter, buyers have room to negotiate seller contributions toward closing costs. That can significantly reduce your out-of-pocket cash needed at closing.

For a broader look at assistance resources, HUD maintains a directory of local buying resources and assistance programs that is worth reviewing.

For more on what first-time buyer programs are available right now, see our first-time home buyer guide for Chester County.

How Your Down Payment Affects Your Mortgage Rate

This is something a lot of buyers do not think about until they are already in the process. Your down payment size directly affects your interest rate on a conventional loan.

Lenders use loan-level price adjustments, or LLPAs, to price conventional loans. These adjustments account for risk factors including your credit score and your loan-to-value ratio, which is how much you are borrowing relative to the home’s value. A buyer putting 20 percent down is a lower risk than a buyer putting 5 percent down. That lower risk translates to better rate pricing.

The difference is not always dramatic but it is real. On a $500,000 loan, even a small rate improvement from a larger down payment can save thousands of dollars over the life of the loan.

This is one of the reasons getting pre-approved early and having a clear picture of your down payment options matters so much in this market. Knowing your options before you start shopping lets you make a strategic decision rather than a reactive one.

For current rate context in this market, see our mortgage rates Chester County page.

Where You Are Buying in Chester County Changes the Math

One thing that makes Chester County unique is that down payment planning cannot be done in a vacuum. The community you are targeting changes the math significantly.

Buyers targeting West Chester are shopping in a market where the median is around $670,000 inside the school district. That price point often requires more cash down to keep the monthly payment manageable and in many cases pushes buyers toward jumbo territory above the $832,750 conforming limit.

Buyers targeting Downingtown have more loan program flexibility at typical price points. Conventional with 5 to 10 percent down works well here and tax rates vary enough by township that property-specific calculations matter.

Buyers targeting Phoenixville often find the most program flexibility of any major Chester County market. Conventional and FHA are both viable and price points give buyers more breathing room on down payment.

Buyers targeting Exton are in a market where strong school districts and highway access keep prices competitive. Similar planning considerations to West Chester in terms of price range and competition.

Buyers targeting Coatesville or Kennett Square have the most options. Lower price points, lighter competition in many cases, and stronger USDA and FHA viability give buyers more flexibility on down payment strategy.

For a direct comparison of how three of the county’s most active markets compare on price and financing, read our West Chester vs Phoenixville vs Downingtown breakdown.

The Right Down Payment Is the One That Works for Your Situation

There is no single right answer on down payment size. I have helped buyers put down 3 percent and buyers put down 30 percent. The right number depends on your savings, your income, your credit, your goals, and the market you are buying in.

What I always tell buyers is this. Do not drain your emergency fund to hit a round down payment number. Keeping three to six months of reserves after closing is important. A home with a larger down payment and no financial cushion is a stressful place to be. A home with a slightly smaller down payment and solid reserves gives you stability.

Getting pre-approved before you decide on a down payment strategy lets me look at your complete financial picture and show you exactly what each scenario looks like for your monthly payment, your PMI obligation if any, and your total cash needs. That conversation usually takes less than 30 minutes and gives you clarity that makes the whole process less stressful.

If you want to know whether now is the right time to buy in Chester County, that guide covers the full picture of market timing, rates, and financial readiness.

About CM Mortgage Services Inc.

I am J.R. Conway, NMLS #147631, and I have been helping buyers finance homes across Exton, West Chester, Downingtown, and the surrounding region for over 20 years. CM Mortgage Services Inc. is a second-generation, family-owned mortgage brokerage located at 1240 West Chester Pike, West Chester, PA 19382. We work with buyers throughout Chester County and offer Conventional, FHA, VA, USDA, Jumbo, DSCR, bank statement, and renovation loan programs so no matter your situation, there is likely a path to approval.

Frequently Asked Questions: Down Payment Chester County PA

How much down payment do I need to buy a home in Chester County PA?

It depends on the loan program. Conventional loans allow as little as 3 percent down for first-time buyers. FHA loans require 3.5 percent down with a 580 credit score or above. VA loans and USDA loans offer zero down payment for eligible buyers. Jumbo loans typically require 10 to 20 percent down. On a $500,000 home in Chester County, a 5 percent conventional down payment is $25,000. Add closing costs and you are typically looking at $35,000 to $45,000 total cash to close.

Do I have to put 20 percent down to buy a home in Chester County?

No. The 20 percent rule is a myth for most buyers. Putting 20 percent down eliminates private mortgage insurance on a conventional loan which saves money each month. But it is not a requirement. Most buyers in Chester County are closing with 3 to 10 percent down depending on their loan program and financial profile.

What are closing costs in Chester County PA?

Closing costs in Chester County typically run between 2 and 4 percent of the purchase price. That includes lender fees, title insurance, Pennsylvania transfer tax which is typically split between buyer and seller, prepaid homeowners insurance, and escrow setup for property taxes. On a $500,000 purchase, plan for roughly $10,000 to $20,000 in closing costs on top of your down payment.

What is the Pennsylvania transfer tax and who pays it?

Pennsylvania charges a transfer tax of 2 percent of the purchase price. In most Chester County transactions this is split evenly between buyer and seller. The buyer typically pays 1 percent. On a $500,000 purchase that is $5,000 for the buyer’s portion. It is one of the larger line items in your closing costs and something to plan for specifically.

Can I get down payment assistance in Chester County PA?

Yes. Fannie Mae HomeReady and Freddie Mac Home Possible both allow 3 percent down with expanded income eligibility. The Pennsylvania Housing Finance Agency offers down payment and closing cost assistance programs for eligible buyers. Seller concessions are also a negotiating tool in lighter competition markets that can reduce your out-of-pocket costs at closing. The availability of specific programs changes so the best way to know what applies to your situation is to have a direct conversation with a local mortgage broker.

Does my down payment size affect my mortgage rate?

Yes. On conventional loans, a larger down payment reduces your loan-to-value ratio which lowers lender risk. That typically results in better rate pricing. A buyer putting 20 percent down will generally qualify for a better rate than a buyer putting 5 percent down with the same credit score. The difference varies but on a large loan amount it can translate to meaningful savings over time.

Ready to Figure Out Your Down Payment Strategy?

If you want to know exactly what your options look like, what the total cash to close number is at your target price point, and which loan program puts you in the best position in the Chester County market, that is exactly the conversation I have with buyers every day.

Start your application here or call us directly at 610-430-6852. I am happy to walk through the numbers with you and build a plan that makes sense for your situation.

All loans subject to approval. Equal Housing Lender.